Posted by Tim Evans in Rooflines, The Shelterforce blog, June 13, 2017 edition. This excerpt copied with permission of the National Housing Institute

While recent news reports have highlighted the low number of affordable housing projects using federal tax credits that are built in high-opportunity areas, a recent examination by New Jersey Future has found that strategic changes in the way federal funds are allocated for affordable housing in the state have meant that many more affordable housing projects have been directed away from high-poverty neighborhoods and toward areas that offer greater economic opportunity.

To evaluate whether those changes had their intended effect, New Jersey Future compared affordable housing projects that received federal Low Income Housing Tax Credits between 2005 and 2012 with projects that received credits between 2013 and 2015, after the New Jersey Housing and Mortgage Finance Agency (NJHMFA), which administers the tax credits in the state, made significant changes to the criteria it uses to award them. The agency made the changes with the specific goal of steering new construction of affordable housing away from areas of concentrated poverty and toward areas where public transit and major job centers existed, and that have higher-performing school districts.

Before the adjustment, a full two-thirds of projects near transit were located in . . .

Okay dear readers, this is a wonky article but for those of you interested in HUD’s Affirmatively Furthering Fair Housing rule it is a good read. (Ted Wimpey)

“For most of the Fair Housing Act’s history, its requirement to “Affirmatively Further Fair Housing” has been largely dormant. With the advent of the new AFFH rules in July 2015, however, there is some promise that this provision might be taken more seriously.”

Beryl Satter knew something like this was bound to happen. Or, rather, to happen again.

The Rutgers historian wrote the book on an obscure form of predatory lending from the mid-20th century that victimized black home buyers when banks would not lend them mortgages. Her book, “Family Properties,” came out in 2009, on the heels of the housing crash. And as she traveled the country talking about it — about families defrauded from the homes they thought they owned, about sellers who promised home ownership but collected deposits and evictions instead — people kept approaching her.

“Pretty much everywhere I go, people say ‘I’ve been hearing about this,'” Satter says. “Contract” lending is making a comeback.

In this model, buyers shut out from conventional lending are offered an alternative: They can make monthly payments on a home directly to the seller, instead of a bank, with the promise of receiving the deed only once the property is entirely paid off, 20 or 30 years down the road. In the meantime, they have few of the legal protections of a typical home buyer but all of the responsibilities of one. They don’t build equity with time. They can be easily evicted. And if that happens, they lose all of their investment.

According to the Detroit Free Press, more homes were bought in Detroit last year using such “land contracts” or “contracts for deeds” than conventional mortgages. In a series of recent stories, the New York Times has reported that Wall Street is now betting on this market, with investors buying foreclosed homes by the thousands and selling them on contract. Earlier this week, the Times reported that the Consumer Financial Protection Bureau is now investigating the practice’s resurgence, although it is not by definition illegal.

What is particularly alarming about the trend, though, is that we’ve seen it before. In its earlier incarnation, it was an explicitly racist form of exploitation. And now it is victimizing the same groups again: mostly lower income and minority home buyers who can’t access traditional credit.

“There’s nothing new here in the slightest,” Satter says. “This is just a continuation of the same old game. That’s what’s so disturbing.”

In the earlier era when this was common, between the 1930s and 1960s, contract lending was in some cities the primary means middle-class blacks had to buy homes. Real estate agents and speculators jacked up the price of properties two- or threefold. Then when families fell behind on a month’s payment or on repairs, they were swiftly evicted. The sellers kept their deposits and found the next family.

Satter’s father, Chicago lawyer Mark Satter, helped organize black Chicagoans to fight the practice in the 1950s. He estimated then that about 85 percent of homes bought by black in Chicago were bought on contract. “It was the way you bought,” Beryl Satter says. “There was no other way.”Many of those families then struggled to keep their homes in a system that was not sustainable by design.

Atlanticwriter Ta-Nehisi Coates based his blockbuster 2014 article “The Case for Reparations”around the story of Chicago blacks who suffered under this system, the outgrowth, as he put it, of a segregated city with “two housing markets — one legitimate and backed by the government, the other lawless and patrolled by predators.”

The Times reports of what’s happening today sound eerily similar. Writers Matthew Goldstein and Alexandra Stevenson report that an estimated 3 million people have bought homes through contracts, although the numbers are hard to track given that the deals are regulated differently in each state and are not subject to the same disclosures as mortgages.

The practice is particularly common, they report, in distressed Midwestern communities like Akron and Detroit, where the government offered hundreds of foreclosed properties to investors in bulk sales. Those same investors, the Times reports, have turned around and sold the properties on contract to moderate-income buyers for sometimes four times as much.

Why now?

But why, though, would a financial scheme created in an era of sanctioned racial discrimination be making a resurgence today? Since Satter’s father tried to sue over the tactic a half-century ago, the Fair Housing Act and Home Mortgage Disclosure Act were passed. And the end of legal discrimination opened up legitimate lending to more blacks who were no longer forced into the housing market’s rapacious underworld.

But a crucial similarity between the two eras exists: Many people still can’t get loans today.

Now, this is the case because lenders have tightened their credit standards since the crash, overcorrecting for the bubble’s exuberance with historic stinginess. The Urban Institute has counted more than 5 million loans currently “missing” from the housing market — mortgages that would have been made between 2009 and 2014 if lenders used the kind of credit standards that were common back in 2001, a benchmark for more reasonable lending prior to the housing bubble.

Millions of Americans over this same time have had their credit ruined by foreclosures — in many cases because of predatory subprime lending that has now put them in the crosshairs of predatory land contracts. Minorities who were disproportionately targeted for the former are not surprisingly concentrated among those caught up in the latter.

“When the banks close down, people still need to buy,” Satter says. And so they find a way. Just as creative investors find a way to meet their demand. Land contracts are to housing whatpayday loans are to banking and Rent-A-Centers are to furniture. What people in need can’t access through credit someone is always willing to provide — for a price.

A lawyer for Harbour Portfolio Advisors in Dallas, one of the larger players in the new wave of contract lending, told the Times that the firm’s business model is “to purchase unproductive residential properties and sell them to other people who will make them productive again.” But Satter frames this differently.

“Choices that black Americans have had for housing loans have been predatory loans, or no loans,” she says. And when banks choose not to loan, she adds, this is who they choose not to loan to.“The result,” Satter says, “is a complete revival of redlining in a slightly different guise.”

This is why she wasn’t surprised to see the practice she’d studied as a historian (and lived through with her family in the 1950s) re-emerge as front-page news.

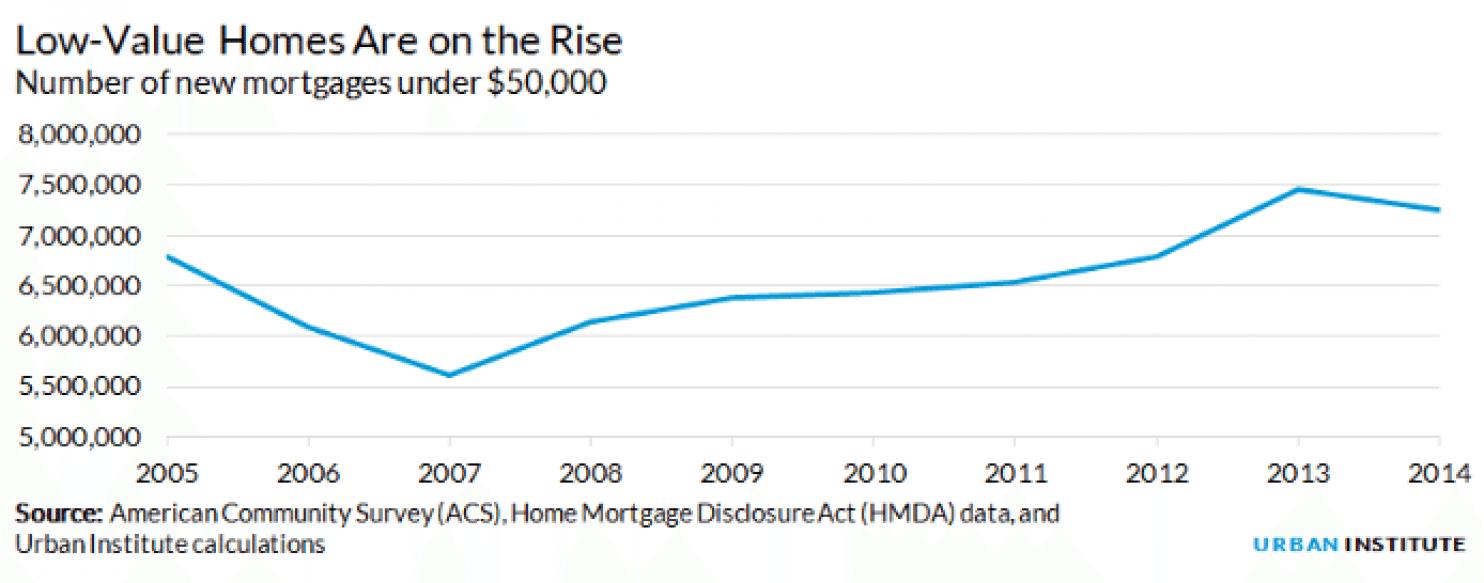

One other factor, though, helps explain why contract selling is back again. The demand among buyers who can’t get mortgages is deep. But so is the supply of houses that might accommodate buyers at the moderate end of the market. The foreclosure crisis created a vast stock of vacant homes, many of which have deteriorated through neglect. Steven Brown, an affiliated scholar at the Urban Institute, has shown that the number of homes worth less than $50,000 has been growing:

Urban Institute

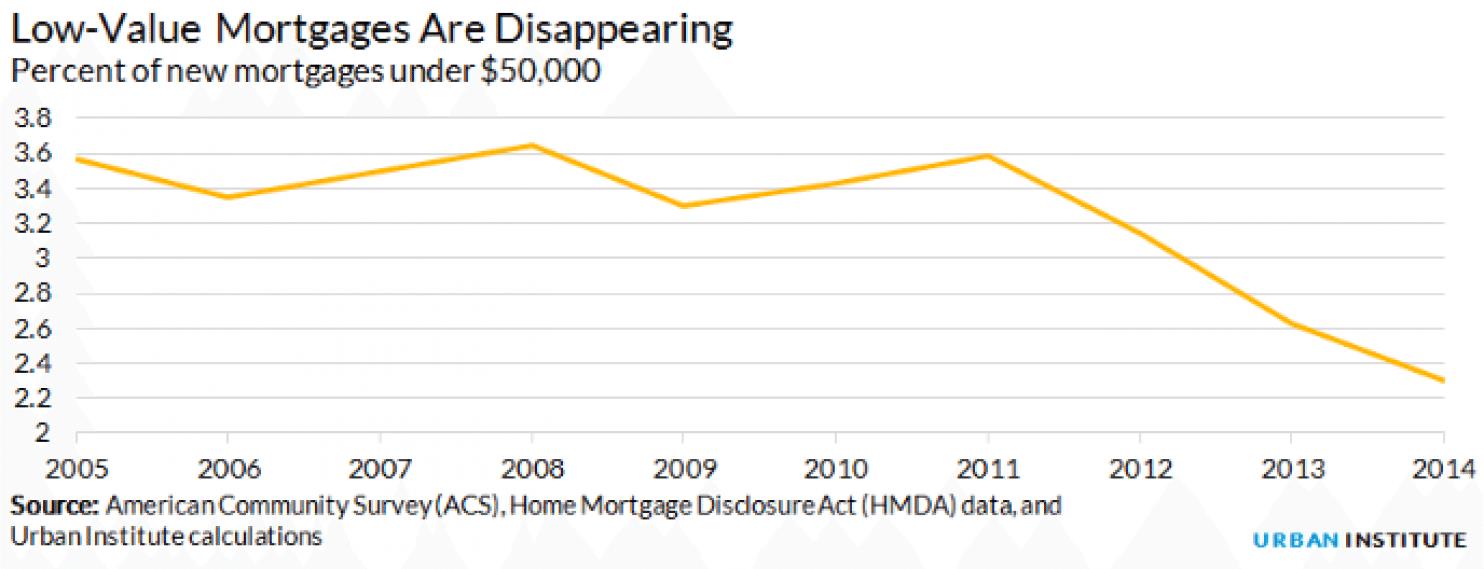

And this has happened as the number of small loans has dwindled:

Urban Institute

So an investor who has bought up thousands of distressed foreclosures for $10,000-$20,000 a piece has to get creative. These properties need expensive repairs, meaning there likely isn’t much profit in repairing and renting them. They aren’t likely to appreciate much over time in stagnant markets like Detroit or Akron, so an investor can’t simply sit on them waiting for a recovery. And these homes can’t easily be sold at a profit to buyers — even with some modest flipping — because buyers in this market can’t get mortgages.

Contract lending, in other words, is just about the most profitable thing an investor could do with these homes. And that opportunity is colliding right now with a time of desperation for would-be buyers.

One way to look at this situation — today or in the 1950s — is that a market failure exists. Something is not working right in the world of legitimate home lending that’s causing families to reach for dubious alternatives, and that’s prompting dangerous models to proliferate. Satter, though, doesn’t see it this way.

“It’s a market success,” she says, viewed from the standpoint of the investors. “They figured out a great way to make a huge amount of money in this situation.”

As for market failures, she says, maybe we should rethink the term. “If you’re looking at how a market works, this is how it works – people saw an opportunity, they came in and grabbed it,” she says. “The market doesn’t care about fair housing for people, or that families need a place to live.”

And that is the other lesson of history that is repeating itself.

I am sharing here in full an article about a U.S. Ninth Circuit Court of Appeals decision with significant fair housing and Affirmatively Furthering Fair Housing import for planning, zoning and permitting of residential housing development that was published April 28, 2016 in the legal issue blog site, “Manatt.” Especially check out the three basic “Practice Pointers” at the end of the article for the main take away.

Avenue 6E Investments, LLC v. City of Yuma (March 25, 2016)

Author: Michael M. Berger

Why It Matters: The Ninth Circuit Court of Appeals reversed a decision in favor of the City of Yuma, Arizona, and concluded instead that there was sufficient evidence to present to a jury that the City had rejected the developer’s application for an increase in zoning density for reasons of barely disguised animus toward the expected residents of the new development. The Court held that issues of disparate treatment and disparate impact under both the 14th Amendment’s Equal Protection Clause and the federal Fair Housing Act needed to be tried.

Facts: The plaintiffs/developers acquired 42 acres of undeveloped land with the intent of building a “moderately priced” housing project. They are known in the area as a developer of Hispanic neighborhoods. Although the General Plan allowed for homes on either 6,000- or 8,000-square-foot lots, a prior owner had it zoned for 8,000-square-foot lots. Unfortunately, the economy would no longer support lots of that size and the developers sought a rezoning to the smaller size which in turn would allow increased density. The City had done some studies, concluding that its population was racially divided, with most of the low-to-moderate-income housing in the areas populated by Hispanics. These developers wanted to develop their housing on the border of a predominantly white area.

The City’s General Plan acknowledged that racial segregation is wrong and that large-lot zoning raises housing costs and impairs the ability of the City to provide housing for moderate-income buyers. The Planning Commission approved the rezoning to smaller lots and recommended that the City Council do so as well. The City Council, however, was besieged with NIMBY complaints and thinly veiled anti-Hispanic charges, complaining that these particular developers were known to “cater to” the people responsible for the vast majority of major crimes.

Two other facts had some import. First, there were similarly priced and modelled homes available elsewhere in Yuma, a fact that the City thought absolved it of any claims of disparate impact. Second, a fact that proved difficult for the City to impress on the Court was that, in the preceding three years, this was the only rezoning request that had been rejected out of 76 applications.

The developers filed suit under the federal Civil Rights Act, 42 U.S.C. § 1983, for violation of the Equal Protection guarantee, as well as for disparate impact and treatment under the Fair Housing Act. The trial court entered summary judgment for the City on the sole ground that the adequate supply of similar housing elsewhere in the City automatically foreclosed any finding of disparate impact.

The Decision: The Court of Appeals reversed. When the opinion began with a paean to the Fair Housing Act and the way it “strikes at the heart of the persistent racism that so deeply troubles our Nation,” something that the provision of more affordable housing can help to cure, it was apparent that the conclusion was foregone: judgment reversed.

The Court of Appeals was unable to disregard the bright light of the fact that out of 76 applications, the only time the City had denied a zone change in the past three years was this one. There could be no explanation for the denial other than racism, particularly in light of some of the communications made by neighbors to the City Council about the presumed criminal proclivities of the anticipated residents of the new development. Nor would the Court have anything to do with the trial court’s idea that the presence of similar developments elsewhere in Yuma obviated the problem. Indeed, it merely emphasized the fact that the City was racially divided and at least some of its residents wanted things to remain that way.

There appeared to be no principled opposition to the requested zone change. As the Court of Appeals put it, the record was replete with “code words” and “veiled references” for the Hispanic influx that the neighbors anticipated, turning the development into a “low-cost, high-crime neighborhood.” The case had no chance on appeal.

Practice Pointers:

Neighbors frequently oppose projects in their neighborhoods that are intended to be occupied by lower-income families. Local governments often bow to this political pressure. This decision may well serve to justify these projects, even in the face of neighbor opposition.

Language similar to the “code words” used by neighbors in this case is common among project opponents opposing higher-density projects. Local agencies need to be mindful of the exposure that this kind of language may impose if the projects are disapproved by the local agency.

At the very least, local agencies need to include sufficient data and facts in the record to support their decision as not being based on discriminatory rhetoric.

A key goal of affirmatively furthering fair housing (AFFH), as it’s envisioned playing out around the country, is to break up concentrations of poverty and to promote socioeconomic and racial integration. That means ensuring opportunities for lower-income people and racial minorities to live in wealthier, “high opportunity” neighborhoods with access to jobs, goods schools and public services.

Two ways to facilitate those opportunities:

Promote regional mobility among people with Section 8 vouchers, enabling them to leave high-poverty areas and move into more well-to-do communities. This can require increasing their housing allowance so that they can afford higher suburban rents.

Build affordable, multifamily rental housing in those same, heretofor exclusive neighborhoods.

Both of these approaches deserve consideration around here, as Vermonters contemplate how to make their communities more socioeconomically inclusive. Meanwhile, it’s interesting to see how they’ve played out in an entirely different environment: metropolitan Baltimore.

First, some background: Baltimore has a long history of racial segregation (click here for a trenchant account), and in the mid-1990s, the Department of Housing and Urban Development was sued by city residents (Thompson vs. HUD) for its failure to eliminate segregation in public housing. In 2005, a federal judge found that HUD had violated the Fair Housing Act by maintaining existing patterns of impoverishment and segregation in the city and by failing to achieve “significant desegregation” in the Baltimore region.

Seven years later, a court-approved settlement resolved the case in a way that anticipated the AFFH rule that HUD issued this past summer.

The settlement called on HUD to continue the Baltimore Mobility Program, begun in 2003 in an earlier settlement phase. The program has provided housing vouchers to more than 2,600 families to move out of poor, segregated neighborhoods and into areas with populations that are less than 10 percent impoverished and less than 30 percent black. The program provides counseling before and after the move and has received high marks from evaluators who cite improved educational and employment outcomes for beneficiaries. A similar regional program is underway in Chicago.

The settlement also called for affordable-housing development in these “high-opportunity” suburban communities – 300 units a year through 2020. To make this happen, HUD was to provide new financial incentives for developers.

Here is where the story takes a dispiriting turn. Three years later, not a single developer has applied for the incentives. No affordable housing projects are even in the pipeline. That’s according to an eye-opening story the other day in the Baltimore Sun.

So, what happened? Why haven’t developers shown any interest? HUD had no explanation, according to the story, which suggested that perhaps the program hadn’t been well-enough publicized: a prominent builder of affordable housing admitted he didn’t even know about the incentives. Could it be that they weren’t generous enough?

Whatever the reason, the Baltimore experience reflects how difficult it can be to introduce affordable housing to privileged enclaves. No one should underestimate the AFFH challenge.

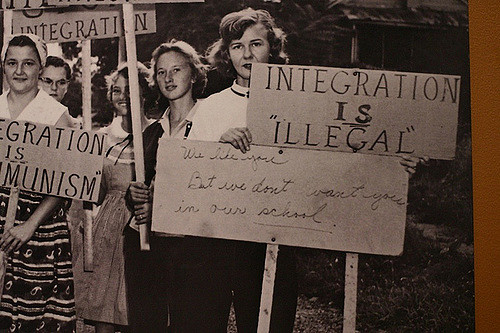

It wasn’t the failure of “forced busing” that led to current racial disparities in school achievement outcomes. The problem, rather, is that the nation’s schools have become more segregated over the last three decades, as integration dropped from the agenda of education policy-makers.

So wrote a Syracuse University education professor, George Theoharis, in an interesting piece in the Washington Post Sunday.

Two startling observations derive from his home town — which happens to be in our neck of the woods.

He notes the enormous disparities in programs, and outcomes, between a middle school with an 85 percent black and Latino student body and another middle school, 10 miles away, that’s 88 percent white. And he points out that in 1989, the city’s schools were about 60 percent white and 20 percent black/Latino, and that now, the district is 28 percent white, 55 percent black/Latino.

Theoharis goes on to discuss how a renewed emphasis on desegregation in educational policy could provide remedies: Redesigning school districts, for example, and putting them together “like pie pieces, so they cut across urban, suburban and even rural spaces”; or creating magnet schools; or providing incentives to school districts to desegregate.

(Note: Magnet schools were the Burlington School District’s remedy for socioeconomic achievement gaps.)

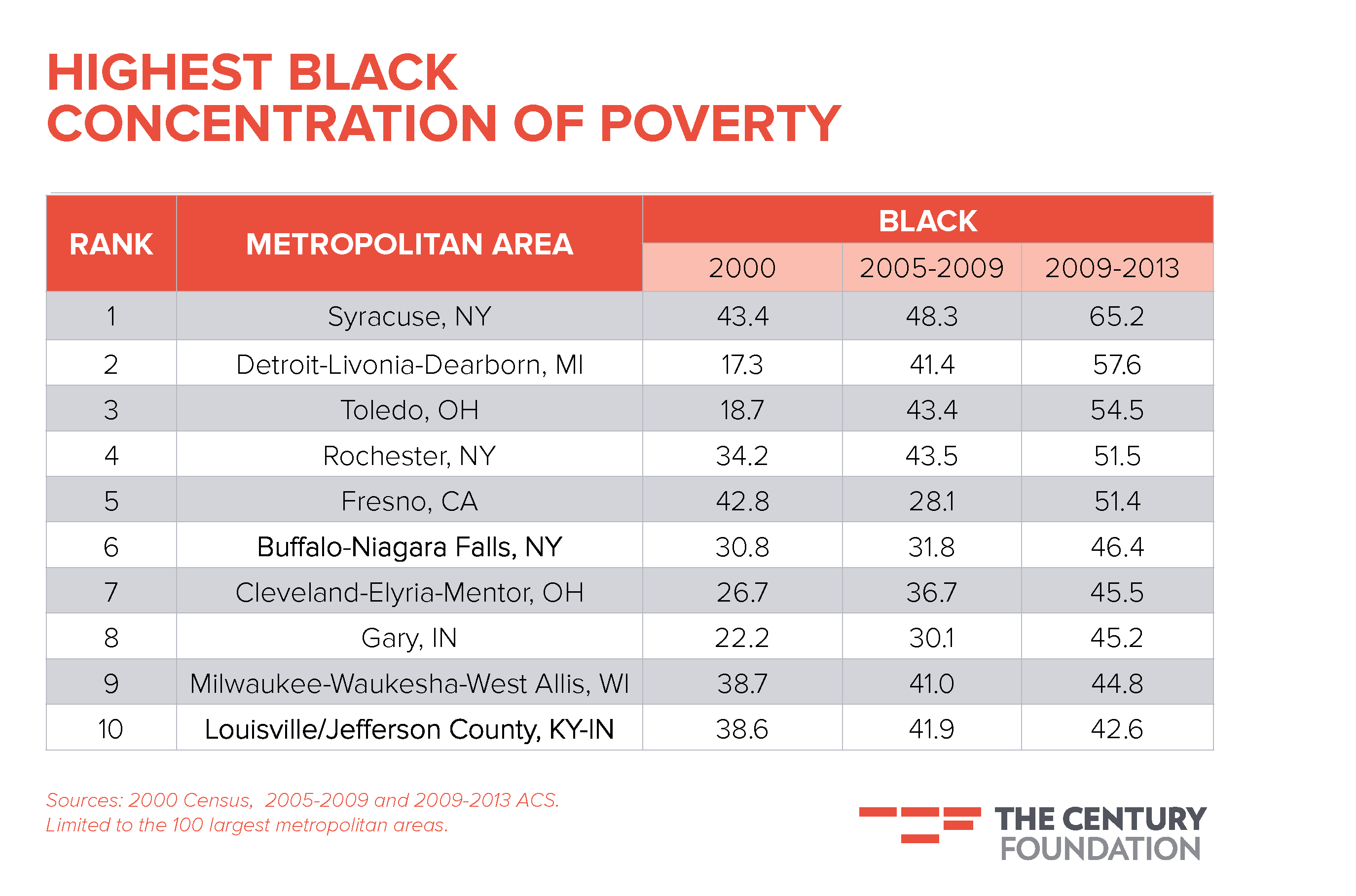

But Theoharis never delves into the heart of the matter: residential segregation. This has grown worse in many cities since 2000, with an increase in the number of high-poverty neighborhoods, as we noted in an earlier blog post citing “The Architecture of Segregation,” a paper that detailed the demographic trends. In Syracuse since 2000, according to that paper, “the number of high-poverty tracts more than doubled, rising from twelve to thirty… As a result, Syracuse now has the highest level of poverty concentration among blacks and Hispanics of the one hundred largest metropolitan areas,” as shown in this table:

The takeaway is that addressing residential segregation iskey to addressing school segregation. Another analysis of school segregation and racial performance disparities, by the Economic Policy Institute’s Richard Rothstein, put it like this:

“Education analysts frequently wonder why a black–white achievement gap remains, even when individual poverty and family characteristics are similar. Partly it’s because of greater (and multigenerational) segregation of black children into neighborhoods of high poverty, few employment opportunities, and frequent violence….

“It is inconceivable to think that education as a civil rights issue can be addressed without addressing residential segregation … Housing policy is school policy; equality of education relies upon eliminating the exclusionary zoning ordinances of white suburbs and subsidizing dispersed housing in those suburbs for low-income African Americans now trapped in central cities.”

Affirmatively furthering fair housing (AFFH) is a recurrent theme on this website, so if you’re still not conversant with the phrase, today’s post is another opportunity. Essentially, the AFFH rule issued by HUD over the summer represents a reinvigorated push to promote inclusive communities and to break up concentrated areas of segregation and poverty that the 1968 Fair Housing Act was intended to dispel.

If for no other reason, you should become familiar with AFFH because it’s a key addition to contemporary American civil rights vocabulary. You can bone up on previous posts here, or here, or delve in to some of this website’s Resources.

And if you’re a citizen committed to supporting affordable housing development in mixed-income, higher opportunity areas, your role may be important than you thought. Consider this excerpt from an essay by Michael Allen, a partner in the civil rights law firm of Relman, Dane & Colfax and one of the leading legal lights nationally in fair housing litigation:

“What HUD produced is a Final Rule long on ‘carrots,’ but painfully short on ‘sticks.’ To compound that problem, HUD does not currently have—and is very unlikely to acquire—sufficient resources to police the compliance of 1200 block grant recipients and 3400 public housing agencies. As a consequence, the promise of the Affirmatively Furthering Fair Housing (AFFH) mandate is likely to be realized only in communities where grassroots and legal advocates mobilize and create their own enforcement strategies. The success of the Final Rule will depend on this grassroots mobilization, on a community-by-community basis, all over the country. That means advocates, collectively, need to step up to the plate and provide the tools and resources for a sustained ‘ground game.’”

As for “carrots” that municipalities can offer for affordable housing development, the Fair Housing Project’s own Ted Wimpey offered a nice summation in his August testimony to the Vermont Advisory Committee to the U.S. Commission on Civil Rights: inclusionary zoning, density bonuses and impact-fee reductions, among others.

It’s not every day that we can praise the New York Times editorial board for following in Thriving Communities’ wake. Saturday’s editorial, which borrows its headline, “The Architecture of Segregation,” from a study we posted about last month. The editorial, while noting this two summer’s “positive” developments – the Supreme Court’s disparate impact decision and HUD’s AFFH rule – rightly takes federal officials to task for failing, over many years, to enforce the Fair Housing Act. And the editorial invokes Walter Mondale’s comments at the HUD conference last week about how the act’s intent is “not fulfilled” by exclusionary land-use planning.

While government deserves a good share of the blame for the present state of residential racial segregation, there are those in the community of fair housing advocates who contend that the real estate industry has been at fault, too. How else to account for the fact that upper-middle-income black families don’t have comparable access to the neighborhoods where their upper-middle-income white family peers live.

Indeed, one factor that may have contributed to segregated patterns is the choice of many whites to opt out of integrated communities, as Stacy Seicshnaydre pointed out in a law journal article last year, “The Fair Housing Choice Myth.” And one way to address that, Seicshnaydre argued, is to defund exclusion — as application of the AFFH rule promises to do, at least in theory.

Meanwhile, HUD conferees were reminded last week, redlining is still with us, and new cases are in the pipeline.

for affirmatively furthering fair housing – good work by the New Jersey Housing and Mortgage Finance Agency (NJHMFA)

for affirmatively furthering fair housing – good work by the New Jersey Housing and Mortgage Finance Agency (NJHMFA)