ft. Emily Collins, Civil Rights Specialist Contractor for The United States Attorney’s Office of the District of Vermont

This guest blog feature is by Emily Collins, a Civil Rights Specialist, Contractor for Vermont’s United States Attorney’s Office . The United States Attorney’s Office is one of the resources available for folks who want to file a complaint about housing discrimination, particularly if there are patterns or practices of discrimination. CVOEO’s Fair Housing project welcomes our partners to add their voices to our Thriving Communities blog. Please send inquiries to fhp@cvoeo.orgContinue reading Understanding Protections Against Sexual Harassments in Housing→

Beryl Satter knew something like this was bound to happen. Or, rather, to happen again.

The Rutgers historian wrote the book on an obscure form of predatory lending from the mid-20th century that victimized black home buyers when banks would not lend them mortgages. Her book, “Family Properties,” came out in 2009, on the heels of the housing crash. And as she traveled the country talking about it — about families defrauded from the homes they thought they owned, about sellers who promised home ownership but collected deposits and evictions instead — people kept approaching her.

“Pretty much everywhere I go, people say ‘I’ve been hearing about this,'” Satter says. “Contract” lending is making a comeback.

In this model, buyers shut out from conventional lending are offered an alternative: They can make monthly payments on a home directly to the seller, instead of a bank, with the promise of receiving the deed only once the property is entirely paid off, 20 or 30 years down the road. In the meantime, they have few of the legal protections of a typical home buyer but all of the responsibilities of one. They don’t build equity with time. They can be easily evicted. And if that happens, they lose all of their investment.

According to the Detroit Free Press, more homes were bought in Detroit last year using such “land contracts” or “contracts for deeds” than conventional mortgages. In a series of recent stories, the New York Times has reported that Wall Street is now betting on this market, with investors buying foreclosed homes by the thousands and selling them on contract. Earlier this week, the Times reported that the Consumer Financial Protection Bureau is now investigating the practice’s resurgence, although it is not by definition illegal.

What is particularly alarming about the trend, though, is that we’ve seen it before. In its earlier incarnation, it was an explicitly racist form of exploitation. And now it is victimizing the same groups again: mostly lower income and minority home buyers who can’t access traditional credit.

“There’s nothing new here in the slightest,” Satter says. “This is just a continuation of the same old game. That’s what’s so disturbing.”

In the earlier era when this was common, between the 1930s and 1960s, contract lending was in some cities the primary means middle-class blacks had to buy homes. Real estate agents and speculators jacked up the price of properties two- or threefold. Then when families fell behind on a month’s payment or on repairs, they were swiftly evicted. The sellers kept their deposits and found the next family.

Satter’s father, Chicago lawyer Mark Satter, helped organize black Chicagoans to fight the practice in the 1950s. He estimated then that about 85 percent of homes bought by black in Chicago were bought on contract. “It was the way you bought,” Beryl Satter says. “There was no other way.”Many of those families then struggled to keep their homes in a system that was not sustainable by design.

Atlanticwriter Ta-Nehisi Coates based his blockbuster 2014 article “The Case for Reparations”around the story of Chicago blacks who suffered under this system, the outgrowth, as he put it, of a segregated city with “two housing markets — one legitimate and backed by the government, the other lawless and patrolled by predators.”

The Times reports of what’s happening today sound eerily similar. Writers Matthew Goldstein and Alexandra Stevenson report that an estimated 3 million people have bought homes through contracts, although the numbers are hard to track given that the deals are regulated differently in each state and are not subject to the same disclosures as mortgages.

The practice is particularly common, they report, in distressed Midwestern communities like Akron and Detroit, where the government offered hundreds of foreclosed properties to investors in bulk sales. Those same investors, the Times reports, have turned around and sold the properties on contract to moderate-income buyers for sometimes four times as much.

Why now?

But why, though, would a financial scheme created in an era of sanctioned racial discrimination be making a resurgence today? Since Satter’s father tried to sue over the tactic a half-century ago, the Fair Housing Act and Home Mortgage Disclosure Act were passed. And the end of legal discrimination opened up legitimate lending to more blacks who were no longer forced into the housing market’s rapacious underworld.

But a crucial similarity between the two eras exists: Many people still can’t get loans today.

Now, this is the case because lenders have tightened their credit standards since the crash, overcorrecting for the bubble’s exuberance with historic stinginess. The Urban Institute has counted more than 5 million loans currently “missing” from the housing market — mortgages that would have been made between 2009 and 2014 if lenders used the kind of credit standards that were common back in 2001, a benchmark for more reasonable lending prior to the housing bubble.

Millions of Americans over this same time have had their credit ruined by foreclosures — in many cases because of predatory subprime lending that has now put them in the crosshairs of predatory land contracts. Minorities who were disproportionately targeted for the former are not surprisingly concentrated among those caught up in the latter.

“When the banks close down, people still need to buy,” Satter says. And so they find a way. Just as creative investors find a way to meet their demand. Land contracts are to housing whatpayday loans are to banking and Rent-A-Centers are to furniture. What people in need can’t access through credit someone is always willing to provide — for a price.

A lawyer for Harbour Portfolio Advisors in Dallas, one of the larger players in the new wave of contract lending, told the Times that the firm’s business model is “to purchase unproductive residential properties and sell them to other people who will make them productive again.” But Satter frames this differently.

“Choices that black Americans have had for housing loans have been predatory loans, or no loans,” she says. And when banks choose not to loan, she adds, this is who they choose not to loan to.“The result,” Satter says, “is a complete revival of redlining in a slightly different guise.”

This is why she wasn’t surprised to see the practice she’d studied as a historian (and lived through with her family in the 1950s) re-emerge as front-page news.

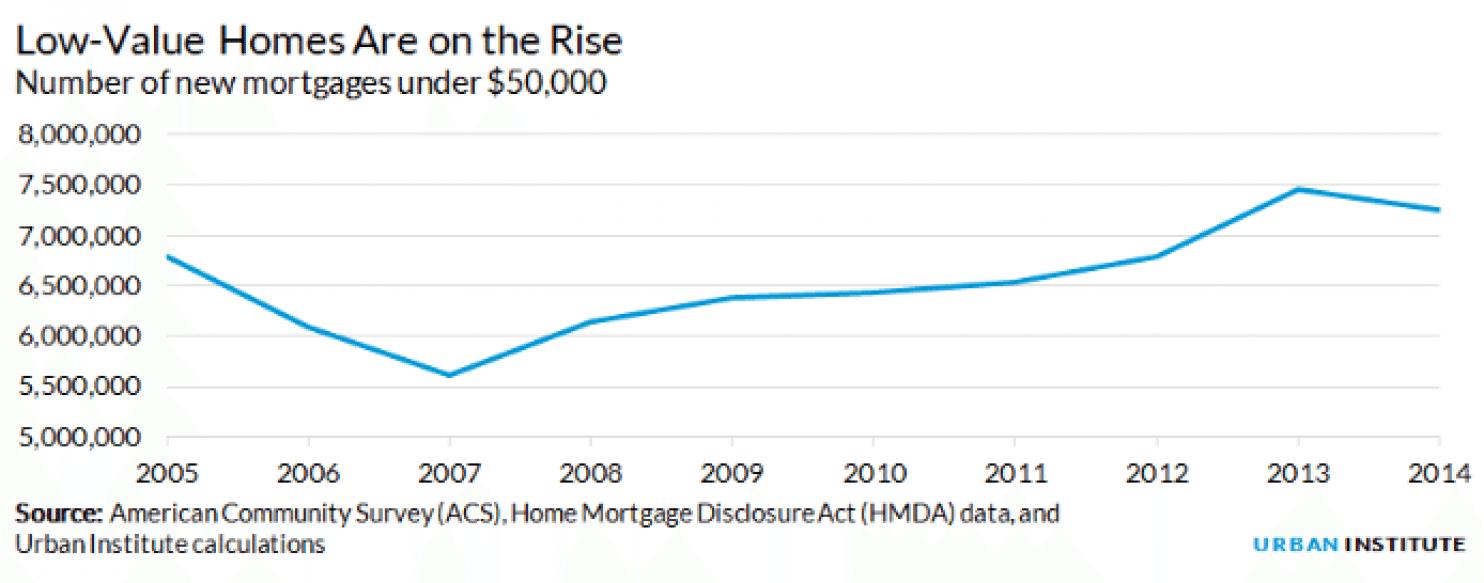

One other factor, though, helps explain why contract selling is back again. The demand among buyers who can’t get mortgages is deep. But so is the supply of houses that might accommodate buyers at the moderate end of the market. The foreclosure crisis created a vast stock of vacant homes, many of which have deteriorated through neglect. Steven Brown, an affiliated scholar at the Urban Institute, has shown that the number of homes worth less than $50,000 has been growing:

Urban Institute

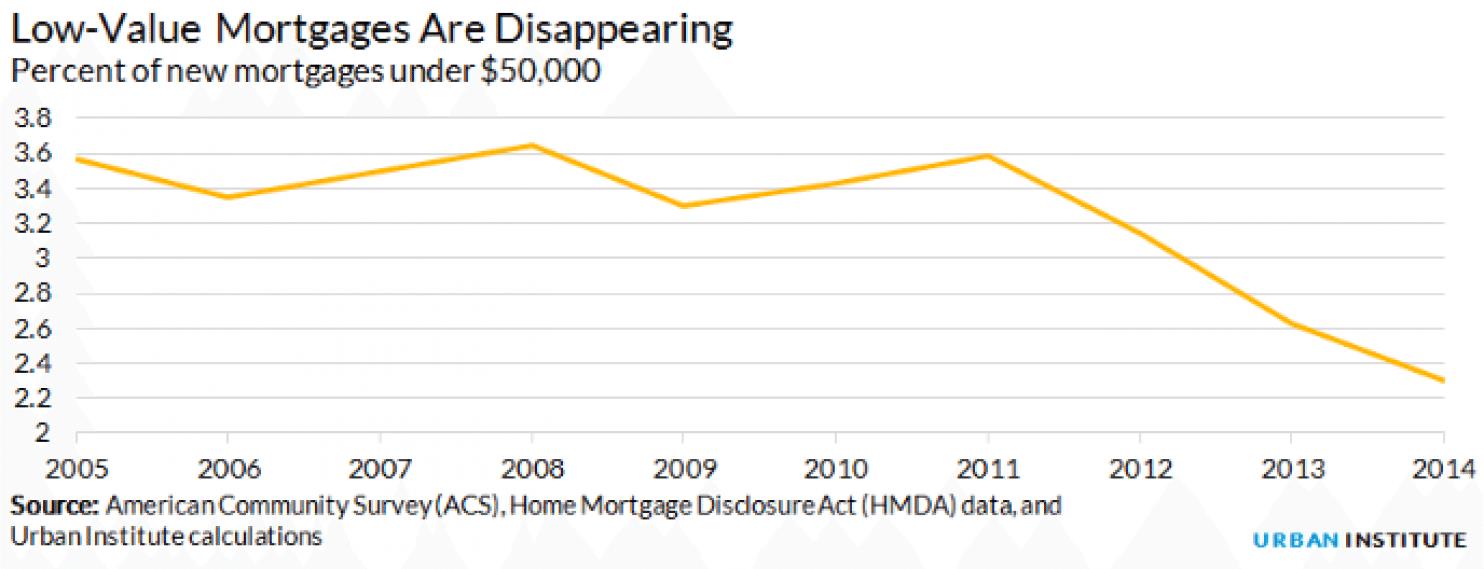

And this has happened as the number of small loans has dwindled:

Urban Institute

So an investor who has bought up thousands of distressed foreclosures for $10,000-$20,000 a piece has to get creative. These properties need expensive repairs, meaning there likely isn’t much profit in repairing and renting them. They aren’t likely to appreciate much over time in stagnant markets like Detroit or Akron, so an investor can’t simply sit on them waiting for a recovery. And these homes can’t easily be sold at a profit to buyers — even with some modest flipping — because buyers in this market can’t get mortgages.

Contract lending, in other words, is just about the most profitable thing an investor could do with these homes. And that opportunity is colliding right now with a time of desperation for would-be buyers.

One way to look at this situation — today or in the 1950s — is that a market failure exists. Something is not working right in the world of legitimate home lending that’s causing families to reach for dubious alternatives, and that’s prompting dangerous models to proliferate. Satter, though, doesn’t see it this way.

“It’s a market success,” she says, viewed from the standpoint of the investors. “They figured out a great way to make a huge amount of money in this situation.”

As for market failures, she says, maybe we should rethink the term. “If you’re looking at how a market works, this is how it works – people saw an opportunity, they came in and grabbed it,” she says. “The market doesn’t care about fair housing for people, or that families need a place to live.”

And that is the other lesson of history that is repeating itself.

ProPublica has a fine expose on racial disparities in debt-collection litigation. Reporters examined court judgments in St. Louis, Chicago and Newark and found that court judgments were twice the size in predominantly black neighborhoods compared to predominantly white neighborhoods – even controlling for income. African Americans significantly more likely than whites to be sued by debt collectors.

So what, you might ask, does this have to with housing, or more particularly, housing discrimination (AKA fair housing)?

Two things:

One inference from the findings is that blacks tend to have less resources – less wealth – to fall back on in hard times. Specifically, they have less wealth in the form of home equity to pass on one from one generation to the next, and that’s a legacy of housing racial discrimination that was promoted and enforced by governments at all levels – and notably, by the federal government from the 1930s on.

As the ProPublic article puts it:

“Experts cite many reasons why blacks might face more lawsuits, foremost among them the immense gap in wealth between blacks and whites in the U.S. It’s a gap that extends back to the institution of slavery and, more recently, to 20th century policies that promoted white homeownership while restricting it for blacks.”

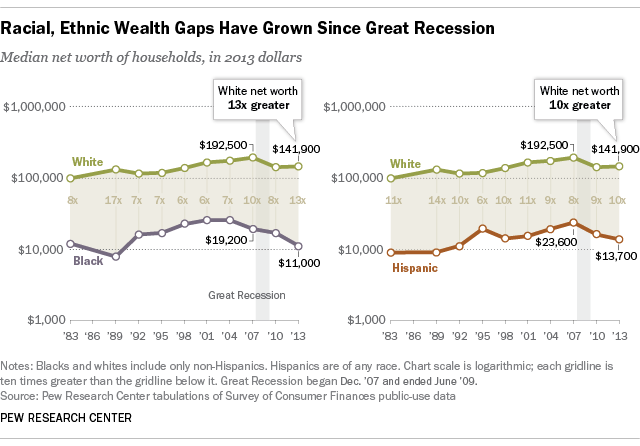

That gap has even widened since the Great Recession, according to the Pew Foundation. The typical black household has a net worth more than 10 times less that of the typical white household:

The other connection to fair housing is that the racial disparity in debt-litigation cases runs parallel to the racial disparity in predatory lending that was revealed during the housing bubble years of the early 2000s. In many areas, blacks were steered to expensive home loans even when they could have qualified for standard mortgage loans. The debt collectors insist they’re treating everyone the same and not screening cases by race. That may be true, but the mass effect is similar to that produced when minorities were are targeted by predatory lenders in the years leading up to the Great Recession.

For a brief description of how a bank was called to account under the Fair Housing Act, check out this synopsis of a case that the civil rights law form Relman, Dane & Colfax filed against Wells Fargo in Baltimore, or this summary in the Baltimore Sun.

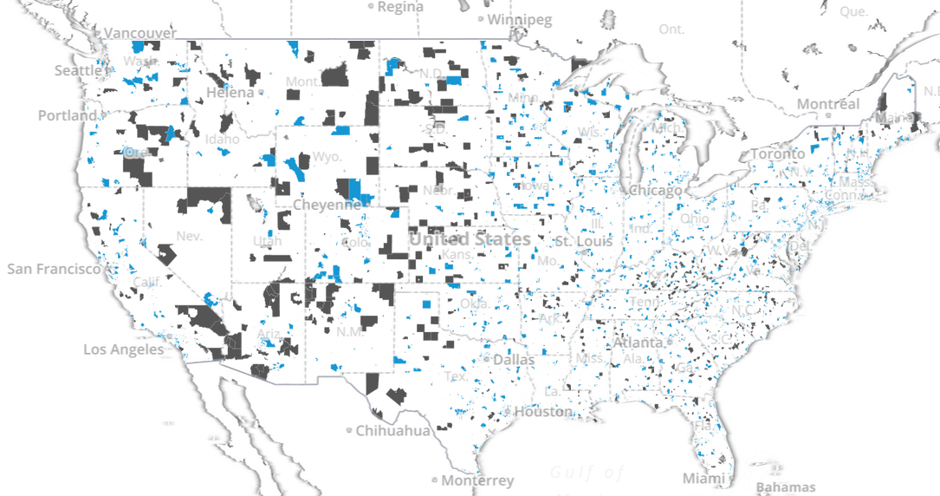

To your library of testimonials on the growing income inequality, you can add this one from the Urban Institute, a study titled “Worlds Apart: Inequality between America’s Most and Least Affluent Neighborhoods,” that shows disparities increasing from 1990 to 2010. This paper uses a composite index (income, educational attainment, home ownership rates, median house value) to identify neighborhoods in the top 10 percent and bottom 10 percent.

You can see them plotted on an interactive national map. Here’s 2010 (blue is “top,” grey “bottom”):

If you scroll to the Northeast you can check out Vermont’s evolution – interesting, but not particularly dramatic.

As is the case with most such national surveys that focus on metropolitan areas, this one analyzes “commuting zones.” In Vermont’s case, that’s a designation of questionable applicability, because it means a zone centered on Burlington with a population of 321,946, more than half the state’s total.

In an appendix, the study lists dozens of commuting zones, each with its “inequality index,” and Burlington comes out OK – somewhere in the middle. Ditto Burlington’s growth of income disparity over 20 years.

Although there has been some shifting of the top and bottom zones across the country, the wealthy zones have remained fairly impregnable. One reason for that, as this analysis of the Urban Institute data emphasizes, is that discriminatory housing policies, such as exclusionary zoning (e.g., large lot sizes) that preserve richer residential enclaves. Multi-family rental housing, affordable or not, is typically missing from these neighborhoods altogether.

Of course, discriminatory land use policies aren’t the sole culprit. High land prices are an obvious deterrent for affordable housing development. Then again, discriminatory policies in many cases may have contributed to the higher prices … a vicious circle.

Elizabeth Warren, the Massachusetts senator, gave a speech Sunday in Boston that the website “Salon” called “the realest talk on race by any American politician.” She delivered her remarks at the Edward M. Kennedy Institute for the United States Senate as part of a “Getting to the Point” lecture series.

She had something to say about violence, about voting, and about economic justice – and economic justice as it relates to housing. Some excerpts:

“For most middle class families in America, buying a home is the number one way to build wealth. It’s a retirement plan-pay off the house and live on Social Security. An investment option-mortgage the house to start a business. It’s a way to help the kids get through college, a safety net if someone gets really sick, and, if all goes well and Grandma and Grandpa can hang on to the house until they die, it’s a way to give the next generation a boost-extra money to move the family up the ladder.

“For much of the 20th Century, that’s how it worked for generation after generation of white Americans – but not black Americans. Entire legal structures were created to prevent African Americans from building economic security through home ownership. Legally-enforced segregation. Restrictive deeds. Redlining. Land contracts. Coming out of the Great Depression, America built a middle class, but systematic discrimination kept most African-American families from being part of it.

“State-sanctioned discrimination wasn’t limited to homeownership. The government enforced discrimination in public accommodations, discrimination in schools, discrimination in credit-it was a long and spiteful list.”

Here we interject that she’s just scratching the surface of the federal government’s tawdry history of promoting residential segregation by race. For an eye-opening summation, check out what Richard Rothstein, of the Economic Policy Institute, had to say at the recent HUD conference in Washington. See the video we posted previously.

We note also the racial disparity in home ownership. In 2010, in Vermont, according to the 2012 “Analysis of Impediments to Fair Housing Choice,” the home-ownership for whites (71.4 percent) was nearly twice that for blacks (32.5 percent).

Warren went on to talk inequality over the last few decades, including the disparate effects of predatory lending that preceded the housing crash:

“Research shows that the legal changes in the civil rights era created new employment and housing opportunities. In the 1960s and the 1970s, African-American men and women began to close the wage gap with white workers, giving millions of black families hope that they might build real wealth.

“But then, Republicans’ trickle-down economic theory arrived. Just as this country was taking the first steps toward economic justice, the Republicans pushed a theory that meant helping the richest people and the most powerful corporations get richer and more powerful. I’ll just do one statistic on this: From 1980 to 2012, GDP continued to rise, but how much of the income growth went to the 90% of America – everyone outside the top 10% – black, white, Latino? None. Zero. Nothing. 100% of all the new income produced in this country over the past 30 years has gone to the top ten percent.

“Today, 90% of Americans see no real wage growth. For African-Americans, who were so far behind earlier in the 20th Century, this means that since the 1980s they have been hit particularly hard. In January of this year, African-American unemployment was 10.3% – more than twice the rate of white unemployment. And, after beginning to make progress during the civil rights era to close the wealth gap between black and white families, in the 1980s the wealth gap exploded, so that from 1984 to 2009, the wealth gap between black and white families tripled.

“The 2008 housing collapse destroyed trillions in family wealth across the country, but the crash hit African-Americans like a punch in the gut. Because middle class black families’ wealth was disproportionately tied up in homeownership and not other forms of savings, these families were hit harder by the housing collapse. But they also got hit harder because of discriminatory lending practices-yes, discriminatory lending practices in the 21st Century. Recently several big banks and other mortgage lenders paid hundreds of millions in fines, admitting that they illegally steered black and Latino borrowers into more expensive mortgages than white borrowers who had similar credit. Tom Perez, who at the time was the Assistant Attorney General for Civil Rights, called it a “racial surtax.” And it’s still happening – earlier this month, the National Fair Housing alliance filed a discrimination complaint against real estate agents in Mississippi after an investigation showed those agents consistently steering white buyers away from interracial neighborhoods and black buyers away from affluent ones. Another investigation showed similar results across our nation’s cities. Housing discrimination alive and well in 2015.”

Monday’s civil rights hearing covered a lot of ground on housing discrimination, but it never got around to advertising. Maybe that’s because illegal ads aren’t as pervasive as they used to be. Signs like this hard seldom seen nowadays:

The newspaper staffers who oversee classified ads are generally savvy – they’ve been brow-beaten by fair housing activists enough over the years to have a pretty good idea what passes muster and what doesn’t. Then again, how much real estate advertising are newspapers getting these days, anyway? Not as much as they used to, sadly.

The most popular advertising venue that lacks editorial oversight, of course, is Craigslist. And that’s what the Fair Housing Project devotes most of its monitoring time to, in its capacity of advertising watchdog.

Craigslist, to its credit, puts a little blurb in each of the entries, “please flag discriminatory housing ads” with a link to a summary of what’s prohibited under the federal Fair Housing Act. Vermont’s Craigslist does not provide any info about Vermont-specific discrimination, however. “Receipt of public assistance” is a protected class in Vermont, which means ads can’t say “No Section 8.”

Very few do, though, even on unfiltered Craigslist. Over the last five months, browsing Vermont rental ads on Craigslist several times a week, we’ve found 30 ads with one or two violations (or probable violations – we’re not an enforcing agency, after all).

About two-thirds of the violations have pertained to familial status – a federally protected category. That means presence of kids. That is, the ads appear to discriminate against families with children.

Much of the discriminatory language might be characterized as subtle. Just about everybody, even the proverbial small-time landlord, knows better than to say “no children.” Instead, they say things like, “best for singles or couples” or “single occupant” or “college students only.”

Roughly one-third of the violations pertain to receipt of public assistance. Here again, the language is less than direct. “Professionals only” … other units “occupied by executives, business owners” … “located in a quiet, professional neighborhood.”

The great majority of real estate ads on Craigslist are fine, at least in fair housing terms. Most advertisers, intentionally or not, abide by this useful guideline for what to put in the ad: Describe the property, not who you want to live there.

Ithaca has about 10,000 fewer people, but the two cities have a few things in common – among them, the university/college presence and predominantly white populations. What’s more, they both happen to be listed in somebody’s “17 Best U.S. Cities for Hippies.”

Here are some of the Ithaca findings that might raise parallel questions in Burlington:

“People with disabilities report higher levels of discrimination and lower levels of housing accommodation than other residents.”

This appears to be the case in Vermont generally, judging from Human Rights Commission reports, but the extent to which it might be true in Burlington is worth a look.

“The City of Ithaca does not currently have a Language Assistance Plan, nor is the need for one mentioned in its 2013 Limited English Proficiency Plan.”

Ithaca’s largest minority population is Asian, and four of the seven languages for which translation services are most needed are Asian. Burlington appears to have a more diverse population of refugees, but the question of how Burlington handles assorted language needs is worth asking. After all, as the Ithaca report notes, “Title VI of the Civil Rights Act of 1964 requires that federal assistance recipients provide language assistance to individuals with limited English proficiency.”

“The obligation of sub-recipients of City Community Development Block Grant/HOME funds to Affirmatively Further Fair Housing (AFFH) is not effectively communicated by the City nor understood by its sub-recipients.”

Well! Dare we suggest that AFFH is not terribly well understood in these parts, either?

“Exclusionary tactics against households who rely on public and private subsidies for housing is prevalent in the City and has a disparate impact on protected classes in Ithaca.”

The report notes that 15 percent of the county’s residents have disabilities, but 40 percent of Housing Choice Voucher recipients (Section 8) have disabilities. Similarly, African Americans comprise 6.5 percent of the county population but 20 percent of the Section 8 population. Fair housing testing showed that discrimination against voucher holders was widespread.

Now in Vermont, housing discrimination against people on public assistance is illegal. How commonly the state’s fair housing law is violated remains an open question, though. What share of Burlington’s Section 8 population is disabled or minority, and how do these people fare in the rental market? Perhaps the city’s next fair housing assessment will address these questions.

Amid all the overarching attention to housing segregation and inclusiveness prompted by HUD’s newlyreleased AFFH rule, we shouldn’t lose sight of housing discrimination at the granular, or individual level. It’s still very much with us, in Vermont and everywhere else. What’s more, there’s a good deal of housing discrimination that goes unreported, as a cursory look at Vermont’s statistics makes clear.

First, the national picture: HUD does an annual report toting up housing discrimination complaints based on seven protected categories in the Fair Housing Act: race, color, national origin, religion, sex, disability, familial status. In the last fiscal year for which data are available, total complaints to HUD and affiliated agencies totaled 8,368, of which 53 percent were based on disability, 28 percent on race, 14 percent on familial status (presence of minor children) and 12 percent on national origin.

Now consider the complaints filed with the Vermont Human Rights Commission. According to the commission’s most recent annual report, there were 41 housing discrimination complaints in Fiscal Year 2014, of which 19 were based on disability, 4 on race/color, 4 on “minor children,” and 1 on national origin.

The numbers in Vermont are pretty low, and the discriminatory profile is a bit different from the that for the nation as a whole. Disability is the major source of complaints here, as elsewhere, but in Vermont just 10 percent of the complaints pertained to race. Granted, Vermont is 95 percent white, but the number seems low for two reasons.

For one thing, hundreds of refugees are arriving in Vermont every year. It seems implausible that they confront no discrimination based in the real-estate rental market based on race, religion or national origin.

For another thing, Vermont Legal Aid’s periodic tests of Vermont’s rental markets show much higher incidences of discrimination than are reflected in the complaint statistics.

In 2012-13, VLA conducted more than 200 tests, using control testers and subject testers of assorted races and national origins expressing interest in renting apartments. “Forty-four percent of the tests conducted either demonstrated overt discrimination against the subject tester or otherwise showed preferential treatment toward the control tester,” the VLA’s report concluded. “(T)here were significant rates of disparate treatment against the subject testers in 46 percent of the national origin tests, 45 percent of the familial status test, 36 percent of the African American race/color tests, and 22 percent of the disability tests.”

So, why aren’t more fair housing complaints filed in Vermont? Perhaps because many tenants don’t know their rights, or because they might fear retaliation. As it happens, protection from retaliation is one the rights they might not be aware of.