Category Archives: elected leaders

ACTION ALERT: Please ask Vermont lawmakers to support the Rental Housing Safety Bill Today!

And another thing

This is the last grant-funded post, so we’ll try to keep it snappy, not sappy. What do we know about housing, anyway? Not a lot, but a good deal more than when we signed on to this gig 10 months ago.

For what they’re worth, we’ll leave you with a gratuitous thought and an anti-climactic ranking.

Housing can’t simply be left to the private market, any more than health care or education. It’s time for people to accept that resolving the housing-affordability crisis will require significant new governmental investment; and alleviating the socioeconomic and racial segregation that continue to stand in the way of fair housing choice, all across the country, will require concerted government intervention. Why shouldn’t the right to decent housing and fair housing choice be a public policy priority commensurate with the right to health care or the right to receive an education?

Rankings abound at New Year, so here’s one with an ancillary question: Rent or buy? 504 counties around the country are listed in order of rental affordability — that is, the percentage of local median income that’s required to pay median rent of three-bedroom apartment in that county. Also listed is the affordability percentage of a median priced home. Compare the percentages to see whether it’s more affordable to rent or buy.

No. 1 in rental affordability (or unaffordability) is Honolulu, at 73 percent. Buy. No. 505 is Huntsville, Ala., at 23 percent. Buy.

You can get to the Excel table by clicking here.

The only Vermont county in the table is Chittenden (listed as Burlington/South Burlington). Sorry, Bellows Falls, Bennington, et al, but that’s the way of these national surveys.

Burlington/South Burlington comes in at No. 152 in rental affordability, at 40 percent. Buying affordability: 46 percent. The recommendation: Rent.

That’s despite the fact that, according to the table, the cost of a 3 BR apartment in Burlington/South Burlington went up 12.2 percent in the last year.

Sounds a little high to us (so much for the 3.3 percent figure we’ve been hearing) but again, what do we know?

Could be worse.

A little holiday cheer

- Portland, Ore., has come up with a new funding source for affordable housing: tourists!

The city council has voted to dedicate a share of the tax on Airbnb-type rentals to the city’s Housing Investment Fund — $1.2 million a year. That’s a drop in the bucket in a city where the affordable housing shortfall amounts to about 24,000 units, but it’s better than nothing.

The city council has voted to dedicate a share of the tax on Airbnb-type rentals to the city’s Housing Investment Fund — $1.2 million a year. That’s a drop in the bucket in a city where the affordable housing shortfall amounts to about 24,000 units, but it’s better than nothing. - Jackson Hole officialdom has agreed to consider a plan that would dial back commercial growth in favor of housing, with density bonuses offered for workforce housing. A citizen campaign bearing slogans like “Housing not hotels” apparently got a receptive hearing.

- The Republican leadership of Howell, N.J., is backing an affordable housing project despite, and in the face of, some unusually ugly civic opposition — in a state where support for affordable housing is typically associated with Democrats.

This profile of courage, in the Atlantic, includes a fine summary of the tortuous (and torturous) fate of affordable housing in New Jersey after the landmark Mount Laurel decisions. Another example of how good intentions and a supportive legal infrastructure are not enough.

This profile of courage, in the Atlantic, includes a fine summary of the tortuous (and torturous) fate of affordable housing in New Jersey after the landmark Mount Laurel decisions. Another example of how good intentions and a supportive legal infrastructure are not enough. - The “recapitalization” of Freddie Mac and Fannie Mae, as proposed by two economists, would direct a flood of new money to the states for affordable housing via the Housing Trust Fund and the Capital Magnet Fund.

Vermont would get $4.6 million a year for affordable housing for 20 years under this scheme. Sounds great, but whether this proposal has any legs is an open question. Some members of Congress would just as soon do away with Freddie Mac and Fannie Mae altogether.

Vermont would get $4.6 million a year for affordable housing for 20 years under this scheme. Sounds great, but whether this proposal has any legs is an open question. Some members of Congress would just as soon do away with Freddie Mac and Fannie Mae altogether. - A community of 15 tiny houses is scheduled to open later this month in Seattle to provide transitional quarters for homeless people. Granted, this isn’t exactly cheerful news, but at least it’s different.

Capital ideas

This country’s shortage of affordable rental units runs into the millions, and Vermont’s is in the thousands. Where’s the money going to come from to build or rehab our way out of this hole? Government spending falls chronically and abysmally short, but there’s a glimmer of hope that a growing fraction of the massive need can come from an unlikely source: private investors.

But first, consider the scale of the need. According to the recent Harvard report on rental housing, 11.4 million renter households are “severely burdened,” paying more than 50 percent of their income for housing. (An additional 9.9 million are simply “burdened,” paying more than 30 percent.)

In Vermont, 26 percent of the 75,000 renter households are severely burdened — that’s 19,500 households living in places that are far beyond their means. And in Burlington, 35 percent of the 9,500 renter households are in that position – about 3,300 households.

The federal government’s primary subsidy for affordable housing development is the Low Income Housing Tax Credit, which produces in about 100,000 affordable rental units a year. Then of course there’s the challenge of maintaining affordability for units whose tax credits expire, a challenge that Vermont’s housing nonprofits and state agencies contend with annually as they marshal limited public resources to preserve the affordability of what’s here. And even though they’ve been largely successful, what’s here isn’t anywhere near enough. Yes, the private market is turning out new rental housing to meet the growing population of renters, but the great majority of those new units are high-end.

A new report from the Urban Land Institute and NeighborWorks America, “Preserving Multifamily Workforce and Affordable Housing,” describes a range of new financing vehicles that seek to create or preserve affordable housing. Sixteen partnerships o investment companies – some new, some well-established — are profiled. One thing they have in common is that they offer returns to their investors– who include philanthropies, university endowments, pension funds and private individuals in the single digits, below what the typical real-estate investor might expect to receive. These entities include private equity funds and two real estate investment trusts (REITs) that focus on affordable multifamily developments.

The hook is that this investment sustains a social good: affordable housing. If “socially responsible investing” is popular among Vermont’s progressive monied class, why can’t affordable housing be one of their fiduciary causes? A creative financier might even find some way to enlist the UVM endowment or the state pension fund in support of affordable housing development.

The report also mentions another possible funding source for affordable housing — the EB-5 program, which pulls in big investments from foreigners (typically from East Asia) in exchange for green cards, and which we’ve harped on before. Yes, EB-5 is supposed to be a job-creation program, but it turns out that real estate development developments are among the most popular EB-5 projects, in part because the construction jobs count. (Check out this article, “Real Estate: Still the Darling of EB-5.”) True, affordable housing isn’t the typical EB-5 project, but it has been done – in San Francisco’s Hunter’s Point Shipyard, and in Seattle, near the Seahawks’ stadium. Next up, Miami.

How about Newport, Vt.?

The Burlington College land deal

Burlington College’s intent to sell off much of its lakeside acreage drew opposition when it was announced two years ago. Now, as a development plan awaits City Council approval, the grumbling continues. Some of the grumblers apparently cling to an obsolete fantasy: namely, that most of the property could be spared development and conserved as greenspace.

Thumbnail history: In 2011 the college bought 32 acres from the Catholic diocese for about $10 million, then came to the realization, after a couple years of stagnant enrollment, that it couldn’t afford the payments. To survive, the college would have to sell off a big chunk of the land, and it revealed its plan to do so to housing developer Eric Farrell a little over two years ago.

The deal wasn’t done, though, and there was a window of many months when someone else — someone like the Nature Conservancy, say, or a land trust — could have stepped forward to offer the $7 million or so that would have been necessary to buy the developable land for conservation purposes. No one did, though. That’s why the greenspace fantasy is obsolete.

Not developing the land was not an option, at least if Burlington College wass to stave off bankruptcy. And if the college were to go belly up, well, then ownership of the property would have reverted to creditors (principally a bank), leading to a development scenario perhaps less palatable than Farrell’s.

If there’s anything reasonably left to grumble about, it’s in the details of the agreement the City Council will review next week. Among those details, as we understand them: The city is acquiring 12 lakeside acres for $2 million to be maintained as parkland (a parcel, by the way that has been appraised at $2.9 million). Farrell will develop about 550 housing units on 16 acres, of which 160 will be affordable to families of income below 65 percent of the median, with other units targeted to people of moderate income, while the rest are market-rate; and 200 beds for students on a parcel the college will retain for its campus.

This much is clear: The city is in desperate need of more affordable housing, and it has its inclusionary zoning ordinance to thank for the affordable units in this scheme, and (2) This inclusive new neighborhood, as planned, will be one of exemplary economic diversity.

Renters arise!

Since 2005, the number of renters in this country has gone up 9 million, to 41 million, the biggest surge of any decade on record. That brings the share of renting households to 37 percent, the highest in half a century. Meanwhile, their rents are up and their incomes are down: From 2001 to 2014, rents rose 7 percent (above inflation) and incomes dropped by 9 percent.

The biggest increase in renter households, surprisingly, came from the Baby Boomer cohort – people in their 50s and 60s. In fact households 40 and older make up the majority of renters.

These are among the findings in “America’s Rental Housing,” a 44-page study out this week from Harvard’s Joint Center for Housing Studies.

Not only are there many more renters, but many more of those renters can’t comfortably afford to live where they do. In 2014, 49 percent of renters were “burdened” (meaning they paid more than 30 percent of their incomes for rent and utilities) and 26 percent were “severely burdened” (more than 50 percent). According to Vermont Housing Data, Vermont’s current rates are a tad higher: 52.5 percent and 26.4 percent.

Yes, the housing burden falls most heavily on low-income people, but it’s growing among the middle-income stratum as well:

“(T)he sharpest growth in cost-burdened shares has been among middle-income households. The share of burdened households with incomes in the $30,000–44,999 range increased from 37 percent in 2001 to 48 percent in 2014, while that of households with incomes of $45,000–74,999 nearly doubled from 12 percent to 21 percent. Regardless of income level, though, the shares of cost-burdened households reached new peaks in 2014 among all but the highest-income renters.”

Meanwhile, only about one-fourth of eligible lower-income households receive housing assistance (Section 8 vouchers are not an entitlement!); funding for HUD’s three biggest rental assistance programs is about the same (corrected for inflation) as it was seven years ago, when the economy crashed; and the HOME program, a major source of federal funding for housing programs, has been cut way back. Private developers continue to add to the multi-family housing supply, but most of the recent additions “serve the higher end of the market,” according to the report. As it happens, high-income households (annual $100,000 or more) represent a small but fast-growing share of the rental market.

The report asserts:

“The challenge now facing the country is to ensure that a sufficient and appropriate supply of rental housing is available for a diversity of households and in a diversity of locations. While the private market has proven capable of expanding the higher-end rental stock, developers have only limited opportunities to meet the needs of lowest income households without subsidies that close the large gap between construction costs and what these renters can afford to pay. In many high-cost markets, moderate-income households face affordability challenges as well.”

“Diversity of locations” is an invocation of AFFH (affirmatively furthering fair housing) and the goal of ensuring that a good share of affordable housing is in “high-opportunity” neighborhoods,” as in what follows:

“Policymakers urgently need to consider the extent and form of housing assistance that can stem the rapid growth in cost burdened households. Beyond affordability, they also need to promote development of a wider range of housing options so that more renter households can find homes that suit their needs and in communities offering good schools and access to jobs. It will take concerted efforts by all levels of government to capitalize on the capabilities of the private and not-for-profit sectors to reach this goal.”

Dare we suggest that concerted efforts have yet to be mounted, or even contemplated, by government at many levels?

Unease Down East

Burlington and Portland, Maine, have a few things in common. They’re the biggest cities in their states, they both pride themselves in their trendy livability (as measured by magazine rankings, food-trucks per capita, those sorts of things), they both experienced negligible development of rental housing for many years, they both worry about gentrifying neighborhoods, and they both have a housing affordability problem.

Portland’s problem might seem a bit more acute, thanks in part to a six-part series in the Portland Press Herald that elaborates on what the mayor-elect calls a “housing crisis.”  The themes echo other crises around the country – soaring rents (up 40 percent over the last five years), stagnant or declining incomes, middle-income renters priced out and fleeing to the burbs.

The themes echo other crises around the country – soaring rents (up 40 percent over the last five years), stagnant or declining incomes, middle-income renters priced out and fleeing to the burbs.

The average two-bedroom apartment in Portland, according to the newspaper, is $1,560. That’s too bad, because an apartment like that is out of reach for anyone with a housing voucher. HUD puts the fair-market rent for a two-bedroom in Portland at $1,074 – which happens to be well below Burlington’s $1,309. What’s more, landlords in Portland can capitalize on the hot rental market by charging non-refundable application fees, which their counterparts in Vermont cannot.

How Portland is going to relieve its “crisis” is an open question. The mayor-elect has appointed a committee. The city is examining municipally owned land with an eye toward potential sites for affordable housing. New developments are supposed to make some units affordable for middle-income renters, but that inclusionary policy apparently doesn’t extend to the working poor. Here, as elsewhere, the remedies seem to pale before the problem.

Extracurricular accommodations

There’s a particular form of workforce housing that’s getting a lot of attention lately: affordable housing for teachers. Much of that attention is being paid in California, of course, where many school districts are having trouble recruiting and retaining teachers who can’t afford the prohibitive housing costs (in Silicon Valley, for example, or San Francisco, where the mayor has announced plans to build 500 affordable units for teachers). Similar plans are afoot in Oakland, San Mateo, L.A.

But housing complexes for teachers have arisen on the East Coast, too, mostly in bigger cities — Newark (pictured), Baltimore and Philadelphia, with a development in Springfield, Mass., in the pipeline. These are projects aimed at Teach for America recruits for these cities — recent college graduates who spend two or three years in public or charter schools before they move on to other pursuits.

Baltimore and Philadelphia, with a development in Springfield, Mass., in the pipeline. These are projects aimed at Teach for America recruits for these cities — recent college graduates who spend two or three years in public or charter schools before they move on to other pursuits.

Not all the teacher-housing initiatives are urban, though. Several counties in North Carolina have provided, or pledged to provide, affordable housing for teachers, as has McDowell County, W. Va., in a project carried out with the American Federation of Teachers. In West Virginia, the hope is that the housing will help attract teachers to a place where they otherwise wouldn’t be inclined to settle.

Other states use housing as a teacher-recruitment tool in different ways. Oklahoma offers low-interest loans, for example. Texas offers mortgage assistance for teachers, and Mississippi subsidizes down-payments and closing costs. These happen to be states with pronounced teacher shortages.

Vermont has a teacher shortage, too — perhaps not as dire as those states’, but a shortage nevertheless. According to the Agency of Education’s “Designated Shortage Areas” for 2015-16, teachers of English, Spanish and special education were needed in all counties, and math teachers were needed in half the counties. Could it be that Vermont’s housing costs are a barrier to teacher recruitment? And if so, would it make sense for school districts — which are being encouraged to merge anyway — to collaborate in finding ways to ease the housing burden?

Another line of argument is that school districts, instead of futzing with housing benefits, should simply pay teachers well enough so that they can afford to live in those districts.

In any case, teacher villages, or housing complexes, come in different forms, and it’s not always clear how they gibe with affirmatively furthering fair housing standards. The one in Newark, for example, has been criticized as an oasis for transient young white professionals in a gentrifying neighborhood. (For a nice overview of these programs in The American Prospect, click here.) Still, Vermont communities would do well to think about how they can make affordable housing available to middle-income people – such as teachers – who are hard pressed to pay market rates.

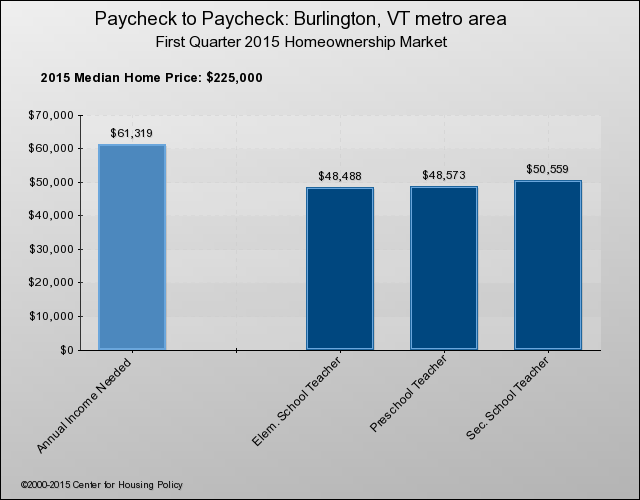

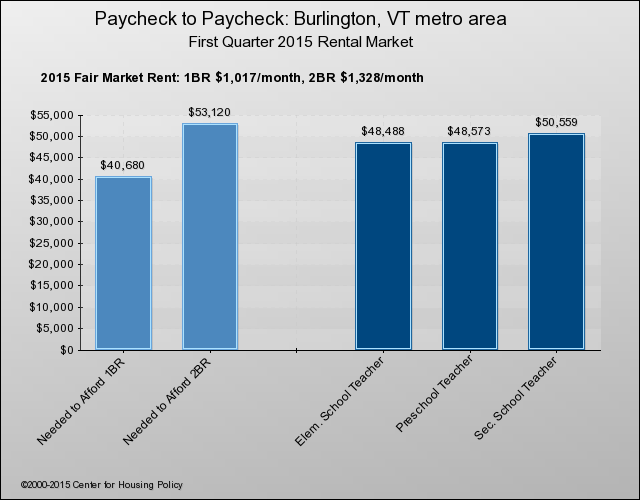

Consider educators in the Burlington metro area. The National Housing Conference’s interactive “Paycheck to Paycheck” matches housing costs (the annual salary needed to afford a house of median price, $225,000) and the salary needed to afford a one-bedroom or two-bedroom apartment.

When you run the model for three educators – preschool, primary and secondary school teachers — you find that:

They can’t comfortably afford the median mortgage…

… or the two-bedroom apartment…

Here a crisis, there a crisis

Never mind California or the Northeast. The housing-unaffordability problem can be found lots of other places, some of them rather unlikely. If you breeze through news coverage from around the country, you can find stories from all over that use the phrase “crisis” or “crunch” or “shortage” to describe the local or regional housing-unaffordability profile:

Just in the past few days, stories have bubbled up from Taos,  Jackson Hole, Aspen, Madison, Asheville, Hawaii, and Austin — all in crisis mode.

Jackson Hole, Aspen, Madison, Asheville, Hawaii, and Austin — all in crisis mode.

Austin is an interesting case: There’s not only an affordability shortage, most of the supposedly affordable units aren’t really affordable after all, according to a rather scathing audit that just came in. From the report summary: “The City does not have an effective strategy to meet its affordable housing needs. Neighborhood Housing and Community Development has not adopted clear goals, established timelines, or developed affordable housing numerical targets to evaluate its efforts in fulfilling the City’s adopted core values. Key information needed to evaluate program effectiveness is incomplete, inaccurate or unavailable.”  This, in the latter-day birthplace of public housing that the mayor pronounced the most economically segregated city in the country.

This, in the latter-day birthplace of public housing that the mayor pronounced the most economically segregated city in the country.

Among the places you might not expect to find a housing crisis: Minot, N.D., rural Iowa,  North Platte, Neb. (Say it ain’t so, North Platte!) And to think that this is not something the presidential candidates can even be bothered to talk about!

North Platte, Neb. (Say it ain’t so, North Platte!) And to think that this is not something the presidential candidates can even be bothered to talk about!

In fact, every county in the country can be said to be in crisis when it comes to housing extremely low-income households (that is, households with less than 30 percent of median income, 11.3 million nationwide). No county has enough units for such people, according to an analysis the Urban Institute did this summer. For an interactive map that will show you how many affordable units in each county for 100 poor households, click here. In Vermont, Orange, Windsor and Windham counties come out the best, with 49 affordable units for 100 households; Caledonia, Lamoille and Orleans have the fewest, at 29. The national average: 28.

Of course, the national challenge is not just to create plenty more affordable housing but to locate it judiciously. New housing options have to be provided for low-income people in low-poverty neighborhoods, otherwise known as “high-opportunity” areas. That’s what affirmatively furthering fair housing is about — breaking up historic settlement patterns of concentrated poverty and segregation and promoting integration.

Naturally, AFFH generates pushback. So, sprinkled among the wash of “housing crisis” stories are accounts of resistance to affordable housing projects in well-healed suburbs – such as Simsbury, Conn. (median household income$104,000) , and Wilmette, Ill. ($127,000).